Experts Say Universal Basic Income Would Boost US Economy by Staggering $2.5 Trillion

a $2.48 trillion increase in the nation's GDP after eight years of UBI. ....... In recent months, everyone from Elon Musk to Sir Richard Branson has come out in favor of universal basic income (UBI), a system in which every person receives a regular payment simply for being alive. ......... a “basic income” of $1,000 per month given to every adult, a “base income” of $500 per month given to every adult, and a “child allowance” of $250 per month for every child. The researchers concluded that the larger the sum, the more significant the positive economic impact. ...... the $1,000 basic income would grow the economy by 12.56 percent over the course of eight years ........ the researchers assumed that the UBI in the U.S. would be funded by increasing the federal deficit

How India Is Moving Toward a Digital-First Economy

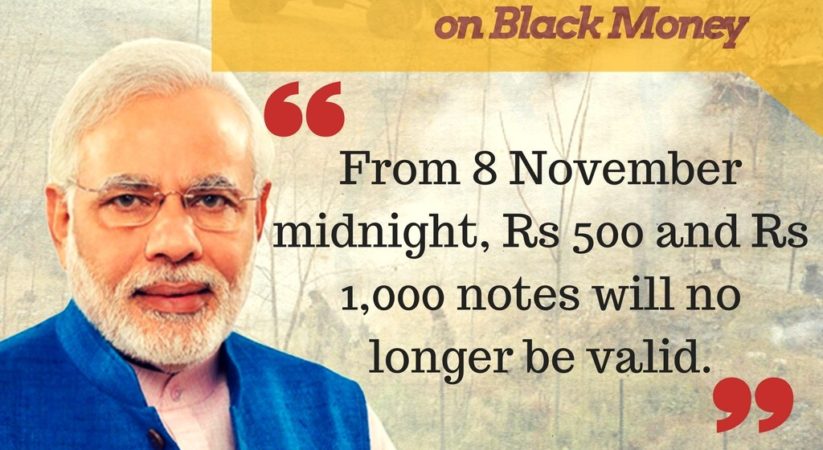

On November 8, 2016, India’s government did something that no other government had attempted before at the same scale: It decided to remove 86% of the country’s currency notes by value from circulation. Over the months that followed, more than 1 billion people participated in a “reboot” of the country’s financial and monetary system. .......... a threshold moment in India’s digital transformation. .......... a government payment system created in 2016 that was processing 100,000 transactions per month in October of that year, prior to the sudden demonetization. A year later, after demonetization, the same system is processing 76 million transactions per month. ........ the country’s economy is operating with $45 billion less cash than it did prior to demonization ......... the largest-scale tax reform ever implemented at a single time: the replacement of a complex web of 17 different taxes with a single Goods and Services Tax (GST). ......... in the first month after the introduction of the GST, over 1 million businesses registered with the system. In only the first few weeks after implementation, the increased transparency and digital data availability that are integral to the GST began to open up new sources of lending to small and medium-size enterprises (SMEs). .......... the “India Stack.” ........ At the base of the stack — and thus at the beginning of India’s story of digital transformation — is a nationwide system of digital identity, generically termed the UID (Unique Identification) system, but more often in India referred to by its project name, Aadhaar. ........ Of the systems that have broken the 1-billion-user mark, many originated in the U.S. and are private-sector efforts — Facebook and Google being among the prominent examples. An exception is Aadhaar, which means “foundation” or “base” in a number of Indian languages, including Hindi. ........ Aadhaar is both the only non-U.S. technical system globally to have broken the 1-billion-user threshold and the only such system to have been developed by the public sector. ....... Aadhaar has the distinction of having reached 1 billion users the fastest; the services built on Aadhaar, through the interoperability that defines the India Stack have, in turn, built their own record of scale and scope. ......... India launched Aadhaar in 2009 with the then-improbable goal of giving every Indian a single digital identity in the form of a biometric authenticated 12-digit number. ....... a unique number based upon de-duplication of the applicants’ biometric information, their submitted iris scans and fingerprints. ....... the search for a “killer app” to prove the value of Aadhaar was elusive. While the ability to authenticate identity was now digital, bank accounts and payment systems were still paper-based — requiring separate and laborious Know Your Customer validation procedures that had the result of continuing to exclude a majority of people in India from accessing the benefits of banking. ........ Modi not only backed the system developed by the previous government but also dramatically increased its funding, broadened its scope, and — most important — amplified its impact. ........ Among the first actions the Modi government undertook was to launch the Pradhan Mantri Jan–Dhan Yojana (PMJDY, or Jan Dhan) financial inclusion program on August 28, 2014. On the very first day that Jan Dhan was implemented, the government created 10 million bank accounts using existing Aadhaar IDs in a paperless manner, at a fraction of the minimum previous customer acquisition costs. Since then, the government has created more than 300 million new, no-frills bank accounts. In additional to a free, zero-balance account, the Jan Dhan provides accident insurance coverage of 100,000 rupees (about US$1,500), along with an overdraft facility of 5,000 rupees (US$80) available for account holders — the point being to incentivize people to participate in the formal banking system. ......... Having a biometrically-verifiable identity number and a bank account created the potential for adding another layer to the service stack: mobile payments. With an identity to create a bank account, and a bank account to receive funds, the hundreds of millions of people eligible for the receipt of government services in India suddenly had a way to access those services digitally, from beginning to end. In India this digital infrastructure is nicknamed the “JAM” trinity, referring to innovative interlinking of Jan Dhan (low-cost bank accounts), Aadhaar (identity), and mobile numbers. The India Stack could now have four layers: an identity layer, a documents layer, a payments layer, and a transactions layer. ......... To understand the human impact of these changes, consider the plight of a mother in an Indian village who is eligible for a government subsidy to send her two daughters to school. Until less than two years ago, in order to avail herself of those funds she would have needed to fill out a form verifying her daughters’ attendance, get that form validated by the school, and bring that form to a government office. Assuming there were no impediments in the processing of the form — a big assumption — she would then have waited as the form traveled up the system to the point when a check would be issued to her in the amount of her benefits. To collect the check she would have needed to travel to a government office. If there turned out to be corruption in the office, she would have needed to produce a sum in cash equal to 15%–20% of the total amount before finally receiving the check. Then, of course, she would have needed to travel to a bank to cash the check. In the end, of the 2,000 rupees to which she was entitled, she would (in a good outcome) have received about 1,400 rupees, with the balance having gone to travel and corruption money........... If we consider this same situation using India Stack, the mother can use a tablet or smartphone to validate her identity using her Aadhaar number in the office of her daughters’ school. Her eligibility for the program is already in the system, and her Aadhaar number is now linked to the zero-balance bank account created for her under the Jan Dhan financial inclusion program. The workflow approves her request in a batch process. Within 24 to 48 hours she gets an alert on her phone that the full 2,000-rupee amount has been transferred to her bank account. ............ the India Stack is envisioned as new social infrastructure with the capacity to increase the resilience of Indian society to change, and thus to help propel India into the 21st-century digital economy. The deployment of the India Stack was one significant precondition for major structural reforms undertaken by the Modi government. This brings us back to demonetization and implementation of tax reforms. ........ The idea of accomplishing a dramatic shift in the nature of the economy with a set of suddenly implemented policies is not new. The “shock therapy” programs of the early 1990s, intended to accomplish the shift from socialist to market economies in Eastern Europe and the former Soviet Union, were based on a similar premise. However, where those programs created an environment in which a few powerful individuals were able to appropriate vast quantities of formerly government-held assets, India’s digital shock therapy has — measurably and verifiably — accomplished the opposite: It has eliminated vast concentrations of “off-the-books” wealth, resetting the clock of development at a more equitable starting point. ........... When India underwent demonetization, the India Stack was suddenly and dramatically thrown into action. India’s own payments corporation launched the BHIM application, a digital payments platform using the Universal Payments Interface underlying the JAM trinity. BHIM became one of fastest-downloaded financial payments applications in recent history. The Universal Payments Interface system is very inclusive, such that it serves both smartphone and non-smartphone users, so every Indian can access banking and make payments digitally. .......... the Indian economy is operating with about $45 billion less cash than if demonetization had not taken place. Banks have far greater liquidity, SME lending is at an all-time high, and digital transactions have multiplied 760 times over in some cases. ......... Prior to the introduction of the GST, companies of any size in India had to keep track of no fewer than 17 different categories of taxes on sales and transactions, including state-level value-added taxes and levies on the interstate transportation of goods. On July 1, 2017, all 17 of those taxes were subsumed into one tax: the GST. ......... an opaque and irrational system that had developed over decades, and that varied across states, was replaced by a simple, transparent system applicable nationwide. ........ India is adding almost 110 million smartphone users every year, and is on the verge of launching Aadhaar-compliant devices with biometric authentication built into phones and tablets. The power of the JAM trinity will come into full force when transactions are enabled using Aadhaar and biometric authentication, creating a system that is not only cashless but cardless. Already, a new entrant into telecommunications service in India has succeeded in using the India Stack to enroll 108 million consumers in 170 days with a totally paperless, mobile-centric manner — in the process achieving customer acquisition costs of less than $1 (USD) per customer, compared with the prior industry standard of $25. ......... India’s development was inequitable and inconsistent for far too long; the country still has a long way to go. The societal challenges created by digital disruption, challenges both expected and unintended, are real. They will be addressed only with a combination of administrative humility and entrepreneurial determination. But the long-term benefits are real. The reality is that India is moving into the future at an unprecedented rate. And the path it is taking to get there is digital.