Milton Friedman, Keynes, and the Great Depression: Economics, Instinct, and Ideological Blindspots

The Great Depression remains one of the most studied economic catastrophes in modern history—precisely because it exposed the limits of prevailing economic orthodoxy, triggered radical political responses, and reshaped the very foundations of macroeconomic thought. It gave rise to Keynesianism, but also inspired enduring critiques from monetarists like Milton Friedman. In this post, we will explore how Friedman would have handled the Great Depression, how Keynes actually did, and why American economists, to this day, exhibit a blind spot when it comes to the U.S. dollar.

What Caused the Great Depression?

The Great Depression wasn't a single event but a chain reaction:

-

The stock market crash of 1929 shattered investor confidence.

-

Bank failures destroyed savings and constricted credit.

-

International trade collapsed under the weight of protectionist tariffs like Smoot-Hawley.

-

Industrial production plummeted, and unemployment in the U.S. soared to 25%.

-

The Federal Reserve’s failure to act exacerbated the downward spiral.

The prevailing economic orthodoxy—rooted in classical laissez-faire thinking—urged governments to "let the market correct itself." But the correction never came. What followed was a decade-long slump and mass misery.

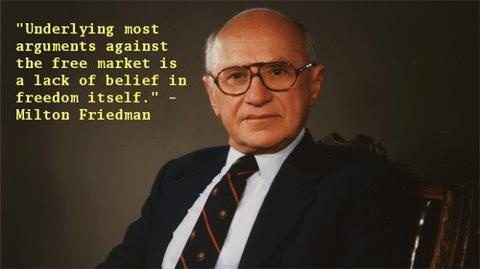

Milton Friedman's Diagnosis: A Monetary Catastrophe

Milton Friedman and Anna Schwartz famously published A Monetary History of the United States in 1963. In it, they argued that the Great Depression was not a failure of capitalism or private enterprise, but a failure of monetary policy. The Federal Reserve, according to Friedman, allowed the money supply to collapse by one-third between 1929 and 1933. This, he argued, turned what could have been a mild recession into a global depression.

“The Great Depression, like most other periods of severe unemployment, was produced by government mismanagement rather than by any inherent instability of the private economy.” — Milton Friedman

Friedman believed that if the Fed had acted as a proper "lender of last resort" and injected liquidity, the depression could have been prevented. His remedy? Expand the money supply aggressively and maintain price stability.

In a world where Friedman had been in charge of the Fed in 1929, he would have pursued expansive monetary policy immediately—buying government securities, cutting interest rates, and flooding the banking system with liquidity. No New Deal. No massive public works. No Keynesian deficit spending. Just monetary stabilization.

But would that have been enough?

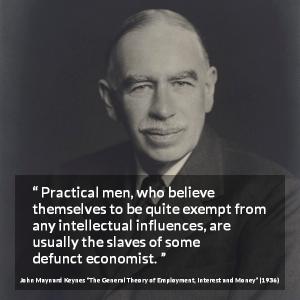

Keynes Responds with a New Paradigm

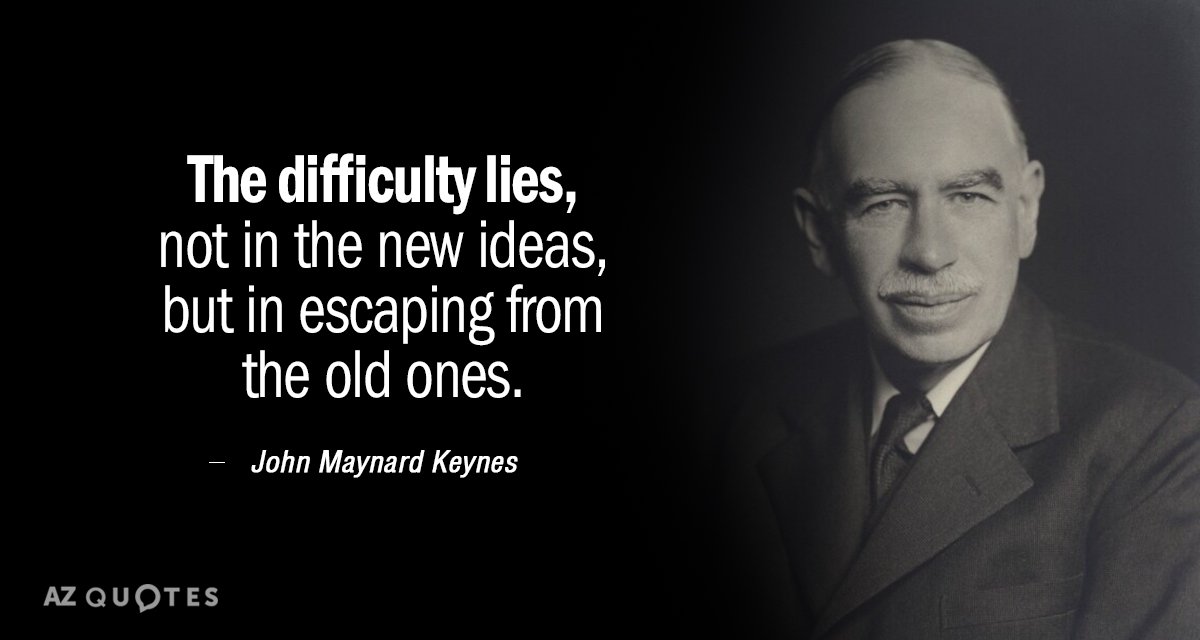

John Maynard Keynes saw something deeper. In a time of collapsing private investment, rising savings, and mass joblessness, merely adjusting the money supply was not going to restore aggregate demand.

Keynes’s insight was revolutionary: in a depression, the economy can settle into a low-output, high-unemployment equilibrium—and stay there. The way out was for the government to spend, not merely to loosen credit. This spending would compensate for private sector retrenchment and stimulate demand.

“The boom, not the slump, is the right time for austerity.” — J.M. Keynes

Franklin Delano Roosevelt (FDR) may not have read The General Theory—it wasn’t published until 1936—but his political instincts aligned with Keynesian logic. Through programs like the CCC, WPA, and public infrastructure investment, Roosevelt injected demand into the economy. The results were uneven but real. Unemployment fell, the economy grew, and a social safety net emerged.

Ironically, it wasn’t until World War II—when deficit spending reached wartime levels—that full employment returned. This vindicated Keynesian ideas more than anything else.

Keynes Again in 2009: Obama’s Stimulus and Beyond

Fast-forward to the Great Recession of 2008–09. The initial response—TARP for banks, then the Obama stimulus—was undeniably Keynesian in spirit. Though not as large as some Keynesians like Paul Krugman wanted, the American Recovery and Reinvestment Act injected over $800 billion into the economy, preventing a total collapse.

Once again, Keynes, not Friedman, offered the more comprehensive diagnosis. The Fed, following a Friedman-style script, slashed interest rates and launched quantitative easing—but with limited effect. It was fiscal policy, not monetary alone, that had the bigger impact.

Would Friedman’s Approach Have Worked in 1929?

Maybe partially. Monetary expansion could have prevented the banking collapses and reduced the initial shock. But without confidence, jobs, or income, people don’t spend. Businesses don’t invest. The economy remains stagnant.

Friedman’s laser-focus on money supply underestimated what Keynes grasped: psychology matters. Fear, uncertainty, and liquidity preference require not just credit, but direct demand stimulus. In that sense, Friedman’s monetarism was necessary—but insufficient.

The Blind Patriotism of American Economists: The Dollar Delusion

One of the most peculiar features of mainstream American economics is the faith in the U.S. dollar as a permanent hegemon. Economists who would scrutinize emerging market currencies under a microscope often treat the dollar with reverence.

Consider:

-

U.S. deficits are dismissed as manageable because the dollar is the world’s reserve currency.

-

The Federal Reserve’s global dominance is assumed as immutable.

-

Calls for de-dollarization or a new international reserve system are treated as fringe or radical.

This isn’t just theoretical bias—it’s intellectual nationalism. Most top American economists have been educated, employed, and published within institutions that are structurally tied to U.S. economic dominance: Harvard, the Fed, IMF, World Bank, Wall Street.

Few dare question whether the “exorbitant privilege” of the dollar could one day fade. Fewer still acknowledge that global dollar dependency creates systemic vulnerabilities—especially for countries in the Global South.

In contrast, Keynes at Bretton Woods proposed a global neutral currency—Bancor—designed to stabilize trade imbalances and reduce reserve currency monopolies. That vision was cast aside by the U.S. in favor of dollar dominance. The consequences are still with us.

Conclusion: Instinct, Theory, and Hegemony

-

Friedman saw the Depression as a monetary failure. He would have saved the banks, but not necessarily the people.

-

Keynes saw it as a failure of aggregate demand—and offered a framework that reshaped modern macroeconomics.

-

FDR, though not formally trained in either school, embodied a Keynesian instinct before it was theory.

-

And today, American economists cling to the dollar as if it were ordained by history, rather than a geopolitical artifact of the 20th century.

To understand and avoid future depressions, we must go beyond domestic theories and monetary dogma. We must recognize the interplay of psychology, demand, global trade, and currency hegemony. Economics is not just math and policy—it is power, politics, and paradigm. And those who fail to question their own hegemonic assumptions may find themselves as outdated as the gold standard they once defended.

मिल्टन फ्रीडमैन, केन्स और महामंदी: अर्थशास्त्र, प्रवृत्ति और वैचारिक पक्षपात

महामंदी (Great Depression) आधुनिक इतिहास की सबसे अधिक अध्ययन की गई आर्थिक आपदाओं में से एक है — क्योंकि इसने तत्कालीन आर्थिक सोच की सीमाओं को उजागर किया, राजनीतिक प्रतिक्रियाओं को झकझोरा और समष्टि अर्थशास्त्र (macroeconomics) की नींव को ही बदल डाला। इसी ने केन्सवाद को जन्म दिया, लेकिन यह मॉनिटरिस्ट मिल्टन फ्रीडमैन की आलोचनाओं की प्रेरणा भी बनी। इस लेख में हम यह विश्लेषण करेंगे कि फ्रीडमैन महामंदी को कैसे संभालते, केन्स ने वास्तव में क्या किया, और आज भी अमेरिकी अर्थशास्त्रियों में डॉलर को लेकर जो अंध भक्ति है, उसका स्रोत क्या है।

महामंदी क्यों हुई?

महामंदी एक अकेली घटना नहीं थी, बल्कि कई संकटों की शृंखला थी:

-

1929 का स्टॉक मार्केट क्रैश जिसने निवेशकों का भरोसा तोड़ दिया।

-

बैंकों का दिवालिया होना जिससे लोगों की बचत नष्ट हो गई और क्रेडिट तंत्र टूट गया।

-

स्मूट-हॉले जैसे संरक्षणवादी टैरिफों ने वैश्विक व्यापार को पंगु बना दिया।

-

औद्योगिक उत्पादन ठप हो गया और अमेरिका में बेरोज़गारी 25% तक पहुँच गई।

-

फेडरल रिजर्व की निष्क्रियता ने इस गिरावट को और गहरा बना दिया।

उस समय की आर्थिक सोच — जो पूरी तरह से मुक्त बाजार पर आधारित थी — कहती थी कि "बाजार स्वयं को संतुलित कर लेगा।" लेकिन ऐसा कभी नहीं हुआ।

मिल्टन फ्रीडमैन का विश्लेषण: मौद्रिक आपदा

मिल्टन फ्रीडमैन और अन्ना श्वार्ट्ज ने 1963 में A Monetary History of the United States प्रकाशित किया। उनका तर्क था कि महामंदी पूंजीवाद या निजी क्षेत्र की विफलता नहीं थी, बल्कि मौद्रिक नीति की विफलता थी। फेडरल रिजर्व ने 1929 से 1933 के बीच मुद्रा आपूर्ति को एक-तिहाई तक सिकुड़ने दिया। इसने एक सामान्य मंदी को महामंदी बना दिया।

“महामंदी, अन्य सभी गम्भीर बेरोज़गारी कालों की तरह, निजी अर्थव्यवस्था की अस्थिरता से नहीं बल्कि सरकार की ग़लत नीतियों से उत्पन्न हुई।” — मिल्टन फ्रीडमैन

फ्रीडमैन की राय थी कि अगर फेड ने "last resort" के रूप में काम किया होता और बैंकिंग प्रणाली में भरपूर नकदी डाली होती, तो संकट टल सकता था। उनके समाधान: मुद्रा आपूर्ति बढ़ाओ, ब्याज दरें घटाओ, बैंकिंग व्यवस्था को बचाओ। लेकिन न तो न्यू डील और न ही सार्वजनिक खर्च की ज़रूरत थी — ऐसा उनका मानना था।

पर क्या यह पर्याप्त होता?

केन्स का उत्तर: एक नई सोच

जॉन मेनार्ड केन्स ने इसे एक अलग दृष्टि से देखा। जब निजी निवेश धराशायी हो गया हो, जनता बचत कर रही हो, और बेरोज़गारी चरम पर हो — तो सिर्फ़ मौद्रिक ढील (monetary easing) से अर्थव्यवस्था नहीं सुधरती।

केन्स की क्रांतिकारी सोच यह थी: एक अर्थव्यवस्था कम उत्पादन और उच्च बेरोज़गारी के स्तर पर अटक सकती है — और वहीं रह सकती है।

इसका समाधान: सरकारी खर्च से मांग को पुनर्जीवित करना।

“मंदी नहीं, बल्कि बूम के समय ही कटौती उपयुक्त होती है।” — जे.एम. केन्स

एफडीआर (Franklin D. Roosevelt) ने शायद The General Theory नहीं पढ़ी थी — वह 1936 में आई — लेकिन उनके राजनीतिक निर्णय पूरी तरह केन्सियन भावना के अनुरूप थे। CCC, WPA जैसी योजनाओं ने काम और वेतन दिए। परिणाम पूर्ण रूप से नहीं, पर स्पष्ट रूप से सकारात्मक रहे। रोजगार बढ़ा, अर्थव्यवस्था में गति आई, और एक सामाजिक सुरक्षा तंत्र की नींव पड़ी।

असल परिवर्तन तो द्वितीय विश्व युद्ध के दौरान हुआ जब सरकार ने युद्ध के लिए भारी खर्च किया — और बेरोज़गारी गायब हो गई। यही केन्स के विचारों का सबसे बड़ा प्रमाण था।

2009 में फिर से केन्स: महामंदी का नया संस्करण

2008–09 की वैश्विक मंदी के समय भी केन्सीय सोच ही आगे आई। ओबामा सरकार का स्टिमुलस पैकेज (लगभग $800 अरब) इस बात का प्रमाण था कि सिर्फ ब्याज दरें घटाना काफी नहीं होता।

फेड ने फ्रीडमैन की शैली में quantitative easing किया, लेकिन जनता में भरोसा और मांग पैदा नहीं हो सकी। वास्तविक प्रभाव सरकार के खर्च से आया — उसी तरह जैसे 1930 के दशक में हुआ था।

क्या फ्रीडमैन का दृष्टिकोण 1929 में काम करता?

शायद आंशिक रूप से। बैंकिंग व्यवस्था को बचाने के लिए मौद्रिक विस्तार उपयोगी होता। लेकिन जब जनता बेरोज़गार हो, भयभीत हो, और पैसे बचा रही हो — तब सस्ती क्रेडिट मदद नहीं करती।

केन्स ने जो बात समझी, फ्रीडमैन ने उसे नज़रअंदाज़ किया: मानव मनोविज्ञान महत्वपूर्ण होता है।

डर, अनिश्चितता और "liquidity preference" को सिर्फ सस्ते ऋण से नहीं, बल्कि सीधी मांग और रोजगार सृजन से ही हल किया जा सकता है।

अमेरिकी अर्थशास्त्रियों का डॉलर के प्रति अंधभक्ति

आज के अमेरिकी अर्थशास्त्री अमेरिकी डॉलर को लेकर गहरा राष्ट्रवादी पक्षपात प्रदर्शित करते हैं।

-

डॉलर को वैश्विक आरक्षित मुद्रा मान कर वे अमेरिका के घाटे को सामान्य मानते हैं।

-

वे मानते हैं कि फेड की वैश्विक प्रभुता स्थायी है।

-

"डॉलर से विमुक्ति" (de-dollarization) को वे हास्यास्पद मानते हैं।

यह केवल बौद्धिक पूर्वाग्रह नहीं, बल्कि संस्थागत राष्ट्रवाद है। हार्वर्ड, फेडरल रिजर्व, वर्ल्ड बैंक और आईएमएफ जैसी संस्थाएं — जो अमेरिकी प्रभुत्व से जुड़ी हैं — वहां से प्रशिक्षित अर्थशास्त्रियों को डॉलर प्रणाली पर सवाल उठाना “अधार्मिक” लगता है।

इसके विपरीत, केन्स ने Bretton Woods सम्मेलन में एक वैश्विक तटस्थ मुद्रा — 'Bancor' का सुझाव दिया था, जो व्यापार संतुलन और मुद्रा अस्थिरता को नियंत्रित करती। लेकिन अमेरिका ने इसे खारिज कर डॉलर को केंद्र में रखा — और आज हम उसी के दुष्परिणाम झेल रहे हैं।

निष्कर्ष: प्रवृत्ति, विचारधारा और प्रभुत्व

-

फ्रीडमैन ने महामंदी को मौद्रिक नीति की विफलता बताया — उन्होंने बैंक बचाए होते, लेकिन आम जनता नहीं।

-

केन्स ने इसे मांग की विफलता कहा — और सरकार की भूमिका को पुनर्परिभाषित किया।

-

एफडीआर ने सिद्धांत नहीं पढ़ा, लेकिन सही निर्णय लिया।

-

और आज के अमेरिकी अर्थशास्त्री डॉलर के मोह में बौद्धिक निष्पक्षता खो चुके हैं।

यदि हमें भविष्य की महामंदियों से बचना है, तो हमें मात्रा नहीं, विचार की क्रांति चाहिए — जो मांग, मनोविज्ञान, वैश्विक व्यापार और शक्ति-संतुलन को समझे। अर्थशास्त्र केवल संख्या या नीति नहीं है — वह सत्ता, राजनीति और दृष्टिकोण का विज्ञान है। और जो अपने ही मुद्रा प्रभुत्व को प्रश्नचिह्न से मुक्त मानते हैं, वे आने वाले बदलावों से सबसे अधिक चकित होंगे।