The U.S. budget deficit and the U.S. trade deficit are two distinct economic measures, but they are interconnected through macroeconomic mechanisms — particularly through national saving and investment balances. Here’s how they relate:

1. Definitions

Budget Deficit: When the U.S. government spends more than it collects in taxes and other revenues. This leads to government borrowing (debt).

Trade Deficit: When the U.S. imports more goods and services than it exports. This is also called the current account deficit.

2. The Twin Deficits Hypothesis

Economists often refer to a theory called the "Twin Deficits Hypothesis", which suggests that a budget deficit can lead to a trade deficit. The logic is:

A larger budget deficit reduces national savings.

If investment demand stays the same, the U.S. must borrow from foreign lenders to make up the shortfall.

This leads to a capital inflow, which causes the dollar to appreciate.

A stronger dollar makes U.S. exports more expensive and imports cheaper, increasing the trade deficit.

If the government increases its deficit (Taxes - Government Spending becomes more negative), and private savings don’t compensate, the trade balance tends to become more negative too.

3. Empirical Reality

Historically, the U.S. has often run both budget and trade deficits simultaneously.

Example: In the 1980s and early 2000s, large U.S. budget deficits (especially under Reagan and Bush) coincided with growing trade deficits.

4. Exceptions and Complications

The relationship is not always 1:1. For instance, during the 1990s, the U.S. ran a budget surplus but still had a trade deficit — due in part to strong private investment and a booming economy.

Global capital flows and exchange rate dynamics also play major roles. Foreign demand for U.S. assets (e.g., Treasury bonds) can finance both deficits.

5. Summary

Budget Deficit ↔ Trade Deficit

Government borrows more → National savings fall

Foreign capital flows in → Dollar strengthens

Strong dollar → Exports fall, imports rise

Result → Trade deficit grows

So, while the budget deficit doesn't cause the trade deficit directly, it contributes to conditions (e.g., lower national savings and stronger dollar) that make a trade deficit more likely.

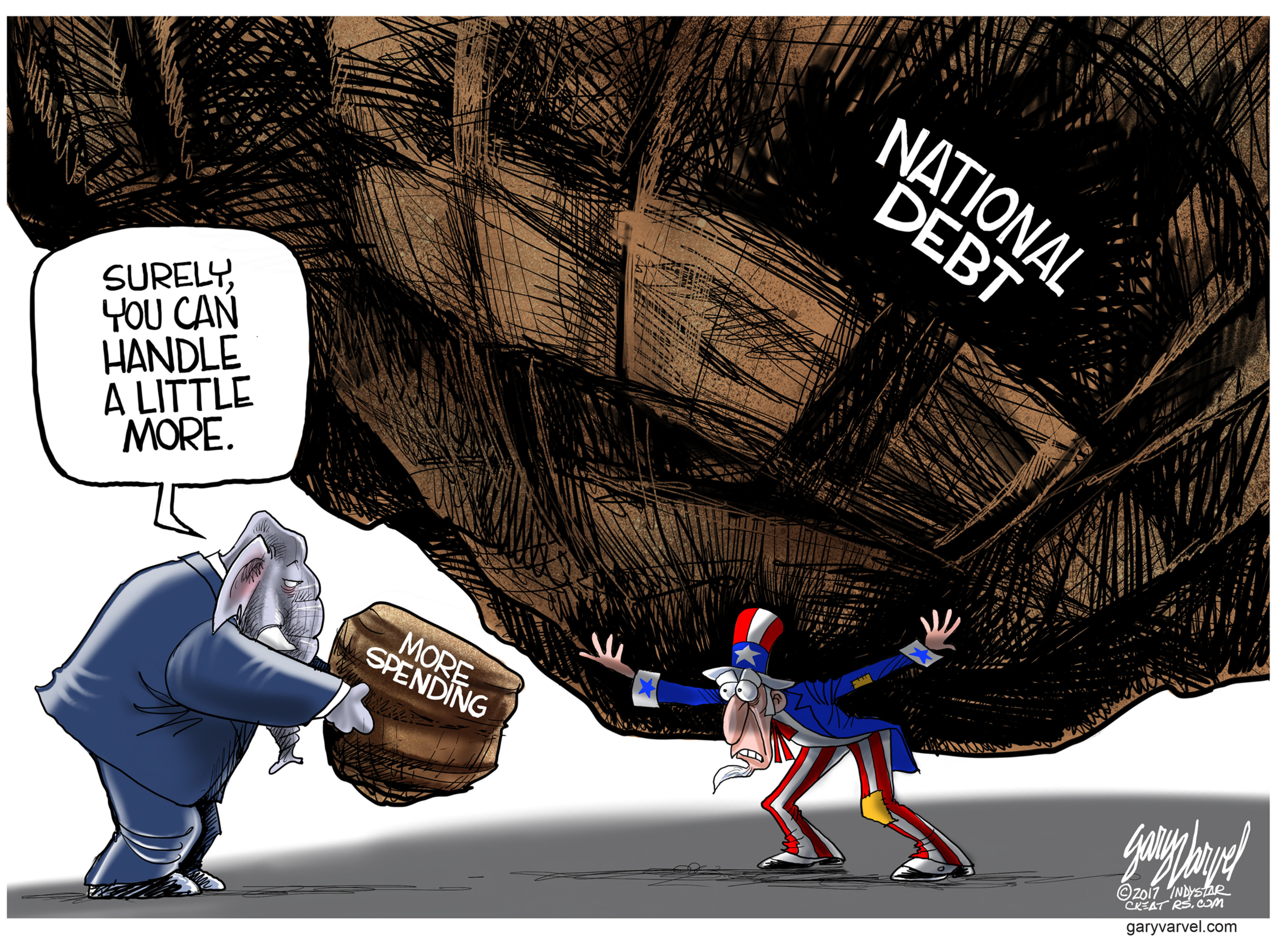

Persistent budget deficits that accumulate into larger and larger national debt have significant implications for the United States—economically, politically, and geopolitically. Below is a breakdown of the key consequences:

I. Economic Implications

1. Higher Interest Payments

As debt grows, the cost of servicing that debt (interest payments) grows too.

In FY2024, interest on the debt is projected to exceed $1 trillion, making it one of the largest single items in the federal budget.

Crowds out other spending (e.g., on education, healthcare, infrastructure).

2. Potential Crowding Out of Private Investment

Government borrowing may compete with private sector borrowing, pushing up interest rates.

This can reduce private investment, leading to slower long-term economic growth.

3. Reduced Fiscal Flexibility

In times of crisis (recession, pandemic, war), the government may have less room to borrow and spend.

High debt can limit policy options during emergencies.

4. Risk of Inflation (In Certain Conditions)

If the government keeps borrowing during a full-employment economy, it may overheat demand and cause inflation.

The Fed may have to raise interest rates, slowing down the economy.

5. Lower Confidence in U.S. Fiscal Sustainability

Investors may begin to demand higher yields on Treasury bonds if they worry about long-term repayment or inflation.

This could raise borrowing costs, even if default risk remains low.

II. Political Implications

1. Rising Partisan Tensions Over Spending

Debt concerns often become a political flashpoint, especially regarding entitlement programs like Social Security and Medicare.

Gridlock over debt ceiling increases can lead to shutdowns or near-defaults.

2. Burden on Future Generations

Children and grandchildren may inherit a heavier fiscal burden, either through higher taxes or reduced public services.

III. Geopolitical Implications

1. Dependence on Foreign Creditors

Foreign countries, particularly China and Japan, own large portions of U.S. debt.

While Treasuries are still considered safe, this creates a geopolitical vulnerability—foreign governments could threaten to reduce purchases.

2. Potential Erosion of Dollar Dominance

Persistent debt combined with trade imbalances could undermine global confidence in the U.S. dollar over the long term.

If confidence in U.S. fiscal discipline erodes, some countries may diversify away from the dollar, affecting its global reserve currency status.

IV. When Is High Debt a Problem?

Debt Isn’t Always Bad

Borrowing during recessions or emergencies is often necessary and helpful.

If debt finances productive investments (infrastructure, education, innovation), it can boost future growth.

But It’s Risky Long-Term If:

Debt rises faster than GDP over time.

A growing share of the budget is consumed by interest payments.

The government loses the political will to adjust course.

V. Verdict

A larger U.S. debt does not guarantee disaster, but it raises long-term risks that must be carefully managed. The key is not just the size of the debt but whether the government can:

The U.S. dollar became the de facto global currency due to a mix of historical events, economic dominance, and structural advantages. Here's a breakdown of the key factors:

1. Bretton Woods System (1944)

After WWII, 44 Allied nations agreed to peg their currencies to the U.S. dollar, which was backed by gold.

The U.S. held the vast majority of global gold reserves, making it the most stable and trusted currency.

Although the gold standard was abandoned in 1971 (Nixon Shock), the dollar's central role persisted.

2. Size and Stability of the U.S. Economy

The U.S. has been the world's largest or second-largest economy for over a century.

It boasts deep, liquid, and open capital markets, especially for U.S. Treasury bonds.

The U.S. political system, despite flaws, has historically offered legal predictability and property protections.

3. Dollar-Denominated Trade

Oil and commodities are mostly priced and traded in dollars (petrodollar system).

Countries need dollars to buy oil, incentivizing them to hold dollar reserves.

Many global contracts and loans (e.g., for developing countries) are in dollars.

4. U.S. Treasury Securities as Safe Assets

Central banks around the world hold U.S. Treasury bonds as a reserve asset because they’re liquid and safe.

The U.S. government has never defaulted on its debt (though political standoffs occasionally threaten it).

This makes dollar-denominated assets the global "safe haven" during crises.

5. Global Confidence and Network Effects

Once the dollar became dominant, it created path dependency—most people and countries use it because others already do.

The dollar is used in over 80% of international trade transactions.

It's held as reserves by most central banks (60%+ of global foreign exchange reserves).

6. U.S. Military and Geopolitical Power

U.S. global military reach and strategic alliances reinforce trust in its system.

The U.S. can enforce sanctions and control access to the dollar-based SWIFT system, giving it powerful leverage.

7. Lack of Viable Alternatives

The euro lacks political and fiscal unity.

The Chinese yuan is not fully convertible and China’s capital markets are not as open.

Gold and cryptocurrencies are too volatile or impractical for most global trade.

Summary:

The U.S. dollar dominates because of a historical head start, economic strength, financial infrastructure, and global trust—not because it's perfect, but because nothing better has yet emerged.

While the U.S. enjoys significant benefits from the dollar’s status as the de facto global currency, there are also serious disadvantages—some subtle, some structural. Here's a breakdown:

🔴 1. Trade Deficits: The "Dollar Trap"

The global demand for dollars forces the U.S. to run persistent trade deficits—it must export dollars to the world.

This often means importing more than it exports, hollowing out U.S. manufacturing over decades.

It’s a paradox: for the world to hold dollars, the U.S. must supply them—usually by buying foreign goods.

Result: Loss of industrial base, fewer manufacturing jobs, regional economic decline.

🔴 2. Strong Dollar Hurts U.S. Exports

Global demand for dollars often drives up its value.

A strong dollar makes U.S. goods more expensive abroad, hurting American exporters.

It also makes imports cheaper, discouraging domestic production.

🔴 3. Asset Bubbles and Financialization

As dollars pour into U.S. capital markets, they inflate asset prices (stocks, bonds, real estate).

Encourages financial speculation over productive investment in infrastructure or R&D.

Increases wealth inequality by enriching those who own capital assets.

🔴 4. Dollar Weaponization Risks Blowback

The U.S. uses the dollar’s dominance for sanctions and financial pressure, which can be effective short-term.

But it incentivizes other countries to create alternatives (e.g. BRICS payment systems, CBDCs, gold settlements).

Overuse could undermine long-term dollar trust.

🔴 5. “Exorbitant Burden” of Responsibility

The U.S. Federal Reserve sets policy for domestic needs—but its decisions impact the entire global economy.

A rate hike to fight U.S. inflation may trigger currency collapses or debt crises in developing countries.

🔴 6. Global Financial Imbalances

The dollar system contributes to a two-tiered global economy where rich countries control currency flows.

It often traps developing countries in dollar debt cycles, requiring austerity or IMF bailouts.

This creates moral pressure on the U.S. to act as a global lender or crisis manager.

🔴 7. False Sense of Security

The U.S. can borrow cheaply because the world demands dollars.

This may encourage fiscal irresponsibility, growing the national debt without immediate consequences.

Eventually, that trust could erode if deficits become unsustainable or if alternatives to the dollar take hold.

Summary:

The U.S. dollar’s global role boosts U.S. financial power—but it comes at a cost to exports, industry, and stability, while inviting backlash from rivals. It’s a double-edged sword: enormous influence, but growing long-term vulnerability.

A multipolar currency world is already emerging. While the U.S. dollar remains dominant, several realistic scenarios point toward a future with multiple global currencies used for trade, reserves, and settlements.

🔄 SCENARIO: A Multipolar Currency System

In this world:

The U.S. dollar still plays a key role.

But the euro, yuan, and others share the stage.

Trade, reserves, and investment flows become more diversified.

Power is more balanced — both economically and politically.

🧭 Key Drivers of Multipolarity

1. Geopolitical Realignments

U.S.-led sanctions (e.g., on Russia and Iran) have pushed countries to seek dollar alternatives.

China and Russia are actively reducing dollar dependence in bilateral trade.

BRICS countries are discussing a common settlement currency backed by a basket of commodities.

2. Technological Disruption (CBDCs & Blockchain)

Central Bank Digital Currencies (CBDCs) from China, India, and others can bypass SWIFT and reduce dollar reliance.

Blockchain-based stablecoins or commodity-backed tokens can settle international trade instantly without needing dollars.

3. Growing Currency Blocs

Euro already accounts for ~20% of global reserves.

The Chinese yuan is being internationalized through the Belt and Road Initiative and swap lines.

Gulf countries and ASEAN are exploring regional payment systems, often linked to local currencies.

4. U.S. Overreach and Trust Erosion

Weaponization of the dollar (e.g., freezing reserves) has made other countries wary.

Holding too many dollars feels risky if geopolitical tensions rise.

🧮 How It Might Work

Use Case

USD

Euro

Yuan

Others

Energy Trade

✓✓✓

✓

✓✓

✓

Reserves

✓✓✓

✓✓

✓

✓

Bilateral Deals

✓✓

✓✓

✓✓✓

✓✓

Tourism/Travel

✓✓✓

✓✓

✓✓

✓✓

Debt Issuance

✓✓✓

✓✓

✓

–

No single currency dominates across all domains. Instead, a flexible ecosystem emerges.

⚠️ Challenges to Multipolarity

Network effects: Most systems, banks, and contracts are dollar-based.

Liquidity: Dollar markets are deep; other currencies can’t yet match.

Trust and convertibility: The yuan, for example, is not fully convertible and China has capital controls.

Political unity: The euro lacks a centralized fiscal union; BRICS lack cohesion.

🔮 Future Scenarios

Gradual Decentralization

Dollar use shrinks slowly; others rise.

CBDCs reduce frictions in non-dollar trade.

Regional Currency Zones

Africa, Latin America, and Asia develop regional currencies or stablecoin networks.

Tokenized Trade & Commodities

Gold-, oil-, or carbon-backed tokens facilitate neutral, trustless settlement systems.

✅ Conclusion

A multipolar currency world is not only possible — it's already forming. The process will be gradual and uneven, but the dollar’s monopoly is weakening, and currency diversity is becoming a strategic imperative in a fragmented, deglobalizing world.

John Maynard Keynes's idea from 1944 may actually have been the best model for global trade: a neutral, global currency not controlled by any single country.

🧠 Keynes’s 1944 Proposal: The Bancor

At the Bretton Woods Conference in 1944, Keynes proposed creating an international clearing union (ICU) with a global unit of account called the bancor.

📌 Key Features:

The bancor would not be a national currency like the dollar or pound.

It would be used only for international trade settlements, not for domestic transactions.

Countries would hold bancor accounts at a global central bank (the ICU).

Trade imbalances would be automatically corrected by penalizing both surplus and deficit countries.

🌐 Why the Bancor Was a Brilliant Idea for Global Trade

1. Neutrality

It avoids giving disproportionate power to one country (as happened with the dollar).

The global economy wouldn't depend on the domestic policy or deficits of the reserve currency issuer.

2. Balanced Trade Incentives

Keynes didn’t just want to punish deficit countries (like IMF austerity does).

He also wanted surplus countries (like China today or the U.S. post-WWII) to spend more or invest abroad to rebalance trade.

This discourages hoarding of foreign reserves and encourages fair trade.

3. No Need for Dollar Hoarding

Developing countries wouldn't need to accumulate billions in dollar reserves "just in case."

Less pressure to run export surpluses purely to get hard currency.

4. Reduced Global Imbalances

The bancor system would have automatic adjustments: limits on how much surplus or deficit a country could build up.

That could prevent crises like the Eurozone imbalance, or the U.S.-China trade gap.

🔴 Why It Didn’t Happen

The U.S., emerging from WWII as the dominant power, rejected it.

It insisted on using the U.S. dollar (tied to gold) as the backbone of the new global financial system.

As a result, global trade became dependent on the monetary and fiscal policy of one country — the U.S.

⚖️ What’s Best for Global Trade Today?

System

Pros

Cons

Dollar Hegemony

Deep liquidity, stability

Biased, creates global imbalances

Multipolar System

Flexibility, competition

Complexity, fragmentation

Bancor/Neutral Currency

Fair, balanced, stable

Needs global governance and trust

In principle, Keynes’s idea remains the most equitable and sustainable — especially in a world of multipolar powers (U.S., China, EU, BRICS). But it would require unprecedented international cooperation and a new global institution to administer it.

🧩 What Could a Modern Bancor Look Like?

Blockchain-based token issued by a global institution (e.g. a reformed IMF or a new BRICS+ clearing union)

Backed by a basket of currencies or commodities

Used only for cross-border settlements

With built-in rules to automatically penalize excessive trade surpluses and deficits

✅ Conclusion

Keynes’s bancor was ahead of its time — a neutral global reserve currency that promotes balanced trade. In an age of dollar fatigue and rising economic nationalism, a modernized version of the bancor could be the ideal framework for fair, sustainable global trade.

The Trump administration's desire to:

Maintain the U.S. dollar’s status as the world’s reserve currency, and

Simultaneously achieve balanced trade with every single country,

is inherently self-defeating. It's a classic case of wanting to have your cake and eat it too.

🧠 Why This Is a Contradiction

🔵 Reserve Currency Role Requires Trade Deficits

For the dollar to function as the world’s primary currency, the U.S. must export dollars to the rest of the world.

That usually happens through running trade deficits—importing more than it exports.

Countries need dollars to buy oil, repay debt, and build reserves. If the U.S. insists on balanced trade with each country, where would the world get those dollars?

🔁 Global dollar demand requires a U.S. trade deficit.

🔴 Bilateral Trade Balancing Undermines the System

The Trump-era strategy of bilateral trade negotiations (vs. multilateral frameworks like the WTO) ignores the reality of multilateral trade imbalances.

A country like Germany may run a big surplus with the U.S., but a deficit with China. The trade system is circular, not bilateral.

Trying to impose 1-to-1 balance with every partner is economically incoherent in a globally networked economy.

⚖️ Example: Dollar Hegemony vs. Balanced Trade

Policy Goal

Implication

Preserve global dollar role

Must keep trade deficits flowing to supply global demand

Balanced trade with all nations

Implies trade surpluses or zero-sum balancing, which would reduce global dollar circulation

They cancel each other out.

🏛️ WTO Dismantling Makes It Worse

The WTO helps manage global trade under predictable rules. Its weakening under Trump increased trade uncertainty and undermined multilateral discipline.

Without a rules-based system, big countries can bully small ones, and currency manipulation and retaliation rise.

Ironically, this undermines trust in the dollar, especially if the U.S. itself is seen as destabilizing global trade norms.

🎯 Bottom Line

Yes — Trump’s trade and currency objectives are deeply at odds:

You can run global deficits to supply the world with dollars, or you can balance trade bilaterally, but not both.

You can dominate a rules-based system, or you can tear it down and go bilateral, but doing both makes the system weaker and less likely to support dollar supremacy.

In short, you can't run a global monetary system and a nationalist trade regime at the same time.

1/ The Trump administration wants two things: 🔹 Preserve the U.S. dollar’s dominance as the global reserve currency 🔹 Achieve balanced trade with every single country That’s like wanting to have your cake and eat it too. 🍰 Here’s why. 🧵#DollarDominance#TradePolicy

— Paramendra Kumar Bhagat (@paramendra) June 30, 2025

7/ The Trump playbook: ✅ Push “America First” trade ✅ Withdraw from or ignore multilateral trade bodies ✅ Demand 1-to-1 trade parity ✅ Maintain dollar supremacy These goals don’t align. At all.#AmericaFirst#TradeContradiction

— Paramendra Kumar Bhagat (@paramendra) June 30, 2025

The dollar is crumbling because of Trump's terrible policies.

But why worry about that, when you could be worrying that American's personal income dropped last month for the first time in over 4 years? pic.twitter.com/SUmu6RoY6V

The Tax Cut Illusion: Why Borrowing Trillions for the Rich Makes No Economic Sense

In a healthy democracy, when a nation runs a budget surplus—meaning it’s taking in more money than it's spending—it naturally sparks a debate. Do we invest in new programs and services that can benefit the public? Or do we return some of that surplus to the taxpayers through tax cuts?

That’s a fair and important debate. One that reflects our values, priorities, and vision for the future.

But what’s happened in recent decades in the United States isn’t that.

What we’ve witnessed instead is a stunning departure from fiscal logic: trillions of dollars borrowed—not during surpluses, but during deficits—from foreign creditors, all in the name of giving tax cuts to the richest individuals and corporations who already have more money than they know what to do with. That’s not just bad policy. That’s dangerous.

When a Surplus Becomes a Missed Opportunity

Let’s start with the idea of a surplus. It means the country has room to breathe—to pay down debt, invest in infrastructure, education, healthcare, or reduce the tax burden responsibly. Think of it like a family that’s finally saved up after years of tight budgets. Do they invest in their kids’ future? Fix the leaky roof? Or do they give a chunk of cash to the wealthiest family member who already owns several homes?

Now flip that on its head. Imagine instead that this family goes deep into debt to give more money to the wealthiest person in the household. That’s what happens when governments cut taxes for the rich while running massive deficits.

Borrowing to Give to Billionaires

When tax cuts are targeted at the ultra-wealthy—people who aren’t lacking investment capital—they don’t inject money into the economy in the same way a middle-class or working-class tax cut might. The rich don’t spend more because they already spend what they want. They don’t suddenly create more businesses because they already have access to capital markets. They mostly just hoard more wealth or buy back their own companies’ stock.

To pay for these tax cuts, the government borrows money—often from foreign nations like China or Japan. That means our children—rich or poor—will be the ones footing the bill through future taxes, higher interest payments, and fewer public services. It’s economic short-termism disguised as strategy.

The Myth of Trickle-Down Economics

The justification for this, of course, is the long-debunked myth of trickle-down economics: the idea that if you give tax breaks to the wealthy, the benefits will eventually “trickle down” to everyone else through job creation and investment.

But the data tells a different story.

Income inequality widens. Wages stagnate. The ultra-wealthy consolidate more power. And the national debt balloons—creating fiscal pressure to cut programs that benefit the majority, like education, healthcare, and retirement security.

Who Really Benefits?

Ask yourself: Who benefits when the U.S. borrows trillions to fund tax cuts for the rich?

Not the middle class. Not small businesses. Not students. Not seniors. Not future generations.

The beneficiaries are a narrow slice of society that already commands an overwhelming share of the nation’s wealth—and whose power grows as government becomes more beholden to their interests through campaign finance and lobbying.

A Broken Logic

Tax cuts can be a smart tool. So can deficit spending—when used wisely during recessions or emergencies, or when investing in long-term growth like clean energy or digital infrastructure.

But borrowing trillions during economic expansions to give tax breaks to billionaires? That doesn’t compute. It’s not economics. It’s not capitalism. It’s plutocracy in disguise.

And we’ll all pay the price. Unless we speak up, vote accordingly, and demand policies that put public good before private greed.

1/ When a country runs a budget surplus, a healthy debate begins: 💰 New public investment? 📉 Tax cuts? If tax cuts win, fine. But what we’ve done instead is borrow trillions—during deficits—to cut taxes for the ultra-rich. How does that compute?#EconTwitter#TaxJustice

— Paramendra Kumar Bhagat (@paramendra) June 30, 2025

False, this bill was never shown to me even once and was passed in the dead of night so fast that almost no one in Congress could even read it! https://t.co/V4ztekqd4g

The "Big, Beautiful Bill" is a term used by President Donald Trump to describe a massive legislative package, officially named the "One Big Beautiful Bill Act," which passed the House of Representatives on May 22, 2025, by a narrow 215-214 vote. It encompasses tax cuts, spending reductions, immigration enforcement, border security, defense spending, and energy policy reforms. Below, we will break down the key components, its size, the likelihood of Senate passage, and a hypothetical revision cutting the bill by 20%, including the option to remove tax cuts.

What is the "Big, Beautiful Bill"?

The bill is a comprehensive Republican-backed package aimed at fulfilling Trump’s campaign promises and agenda. Key elements include:

Tax Cuts:

Extends the 2017 Tax Cuts and Jobs Act provisions, set to expire in 2025, making them permanent.

Eliminates taxes on tips, overtime pay, and auto loan interest.

Boosts the Child Tax Credit to $2,500 per child (2025-2028, then reverts to $2,000).

Increases the federal deduction limit for state and local taxes (SALT) to $40,000.

Enhances the Qualified Business Income (QBI) deduction for pass-through businesses to 23%, though it ends a state-level SALT cap workaround for some businesses.

Provides tax relief for seniors.

Spending Cuts:

Reduces federal spending by $1.2 to $1.5 trillion over a decade, per the Congressional Budget Office (CBO), targeting social safety net programs like Medicaid and SNAP (food stamps).

Freezes states’ provider taxes and prohibits new ones to lower federal costs.

Rolls back some Biden-era clean energy tax credits, including an earlier phase-out of clean energy vehicle credits.

Immigration and Border Security:

Allocates $175 billion for deportations and border wall construction.

Defense and Energy:

Increases defense spending.

Includes energy policy reforms, though specifics vary in reports.

Other Provisions:

Addresses regulatory matters, some of which may face Senate scrutiny under the Byrd Rule (a Senate procedure to ensure budget reconciliation bills focus on fiscal matters).

Size of the Bill

The "size" of the bill can be interpreted in terms of its fiscal impact:

Cost and Deficit Impact:

The CBO estimates the bill reduces federal revenues by $3.7 trillion over 10 years due to tax cuts.

Spending cuts amount to $1.2 to $1.5 trillion over the same period.

Net effect: Adds $2.4 trillion to the federal deficit over a decade, per the CBO.

The Committee for a Responsible Federal Budget suggests a $3.1 trillion debt increase with interest, or up to $5 trillion if temporary tax cuts are made permanent.

Scale:

Described as a $3.8 trillion or $3.9 trillion package in total fiscal impact, reflecting the gross cost of tax cuts and new spending (e.g., $175 billion for deportations and defense).

The legislation itself is over 1,000 pages long, indicating its complexity and breadth.

Will It Pass the Senate?

The bill’s passage in the Senate is uncertain as of June 5, 2025. Here’s the outlook:

Current Status:

The House passed the bill on May 22, 2025, with a 215-214 vote, with two Republicans voting no and one voting present. It’s now under Senate consideration.

Senate Republicans, with a 53-47 majority, aim to pass a revised version by July 4, 2025, using budget reconciliation to avoid a 60-vote filibuster threshold, requiring only a simple majority.

Support and Opposition:

Support: President Trump and Senate Majority Leader John Thune (R-S.D.) are pushing for swift passage, with Trump urging no major changes. The White House claims the bill will drive economic growth and improve fiscal trajectory.

Opposition:

Republican Fiscal Hawks: Senators like Rand Paul (R-Ky.), Ron Johnson (R-Wis.), and others demand deeper spending cuts to offset the $2.4 trillion deficit increase, with some opposing any debt limit hike.

Medicaid Concerns: Sen. Josh Hawley (R-Mo.) and others resist cuts to Medicaid benefits, with Hawley calling such moves “morally wrong and politically suicidal.” Trump has assured no benefit cuts, but changes to provider taxes and copays remain contentious.

Elon Musk: The former head of the Department of Government Efficiency (DOGE) called the bill a “disgusting abomination,” arguing it undercuts spending reduction goals (he targeted $2 trillion in cuts but achieved less).

Democrats: Unified opposition, with Senate Minority Leader Chuck Schumer (D-N.Y.) calling it “ugly to its core,” citing cuts to Medicaid (potentially 8.6 million lose coverage) and SNAP, and tax breaks favoring the wealthy (e.g., $664 billion for the top 1%).

Vote Math: Republicans can afford only three defections with a 53-47 majority, assuming Vice President JD Vance casts a tie-breaking vote. Sens. Paul, Johnson, and others’ resistance could derail it.

Senate Process:

The Senate is “scrubbing” the bill for Byrd Rule compliance, removing non-fiscal provisions (e.g., some regulatory or immigration items). Committees like Senate Finance are revising text, with markups ongoing and a draft expected by mid-June.

Changes are likely, but House Speaker Mike Johnson (R-La.) urges minimal revisions to ensure House re-approval. Significant alterations could force another House vote, complicating the July 4 deadline.

Likelihood: Passage is possible but challenging. GOP unity is strained by deficit hawks, Medicaid concerns, and external pressure from figures like Musk. Democrats’ opposition and the tight timeline add hurdles. Analysts see a narrow path via reconciliation, but substantial revisions or defections could stall or kill the bill.

Redoing the Bill by Cutting 20%

To cut the bill by 20%, we interpret “size” as the total fiscal impact (approximately $3.8 trillion, per some estimates, combining tax cuts and new spending). A 20% reduction means trimming $760 billion over 10 years. We will prioritize removing tax cuts if necessary, while considering spending cuts and other provisions.

Original Bill (Approximate Figures)

Revenue Reduction (Tax Cuts): $3.7 trillion over 10 years (CBO estimate).

Permanent 2017 tax cuts: Major component, exact cost unclear but significant.

No tax on tips, overtime, auto loan interest: Unknown individual cost.

Child Tax Credit boost to $2,500: Temporary, cost not isolated.

SALT deduction increase to $40,000: Unknown cost.

QBI deduction to 23%: Unknown cost, offset by ending SALT workaround.

Spending Cuts: $1.2 to $1.5 trillion over 10 years.

Medicaid, SNAP, and clean energy credit reductions: Bulk of savings.

New Spending:

$175 billion for deportations and border wall.

Defense spending increase: Cost not fully specified.

Net Deficit Increase: $2.4 trillion (CBO), or $3.1 trillion with interest (CRFB).

Total Fiscal Impact: Estimated at $3.8 trillion (gross cost of tax cuts and new spending, before netting out savings).

Strategy for 20% Cut

Target: Reduce $3.8 trillion by 20%, or $760 billion, over 10 years.

Priority: Remove tax cuts first, then adjust spending if needed.

Assumptions: Exact costs of individual provisions (e.g., no tax on tips, SALT increase) aren’t fully detailed in sources, so I’ll estimate and prioritize larger components. New spending (e.g., deportations, defense) is partially quantified, so cuts there are feasible.

Revised Bill

Tax Cuts:

Remove Most Tax Cuts: Eliminate $3.7 trillion in revenue reductions to achieve the bulk of the $760 billion target.

Scrap permanent extension of 2017 tax cuts.

Remove no tax on tips, overtime, and auto loan interest.

Eliminate Child Tax Credit boost (reverts to $2,000, as set to expire in 2025).

Drop SALT deduction increase (stays at current $10,000 cap).

Remove QBI deduction boost to 23% and retain the SALT workaround for pass-through businesses.

Result: Revenue reduction drops from $3.7 trillion to $0, saving $3.7 trillion.

Note: This exceeds the $760 billion target, so we could retain some tax cuts (e.g., no tax on tips) if desired, we will remove all for simplicity and maximum deficit reduction.

Spending Cuts:

Original: $1.2 to $1.5 trillion in reductions.

Retain: Keep these intact to maximize savings and align with fiscal hawk demands.

Medicaid cuts: Controversial, but retained (est. 8.6 million lose coverage).

SNAP reductions: Maintained.

Clean energy credit rollbacks: Kept.

New Adjustment: No additional cuts needed, as tax cut removal overshoots the target. However, to balance concerns (e.g., Sen. Hawley’s Medicaid stance), consider freezing cuts at $1.2 trillion (lower CBO estimate) and avoiding direct benefit reductions, focusing on provider taxes and administrative savings.

Result: $1.2 trillion in savings over 10 years.

New Spending:

Original: $175 billion for deportations and wall, plus unspecified defense increases.

Cut 20%: Reduce by 20% to align with the bill’s overall reduction goal, even though tax cuts already cover the $760 billion.

Original: $3.8 trillion (gross tax cuts and new spending, per some reports).

Revised: $220 billion (new spending only, as tax cuts are gone), a reduction of $3.58 trillion, far exceeding the 20% ($760 billion) target.

Adjustment: To hit 20% precisely, reintroduce a smaller tax cut, e.g., no tax on tips or a modest Child Tax Credit boost, costing ~$500 billion, so total impact is $3.04 trillion ($3.8 trillion × 0.8).

Final Revised Bill:

Tax Cuts: Minimal, e.g., no tax on tips (est. $500 billion cost, a rough placeholder).

Spending Cuts: $1.2 trillion (Medicaid, SNAP, clean energy credits, focused on admin savings).

New Spending: $220 billion ($140 billion for deportations/wall, $80 billion for defense).

Total Fiscal Impact: $500 billion (tax cuts) + $220 billion (new spending) = $720 billion, before cuts.

New Size: $720 billion in gross impact (tax cuts + new spending), a 20%+ reduction from $3.8 trillion.

Caveats

Exact costs of individual tax cuts (e.g., tips, SALT) and defense spending aren’t fully specified in sources, so estimates are approximate.

A 20% cut to a $3.8 trillion bill yields $3.04 trillion, but removing all tax cuts ($3.7 trillion) overshoots. I reintroduced a modest tax cut to align closer to the target.

Senate feedback (e.g., no Medicaid benefit cuts) and Byrd Rule compliance may require further tweaks.

Summary

Original Bill: A $3.8 trillion package with $3.7 trillion in tax cuts, $1.2-$1.5 trillion in spending cuts, and ~$275 billion in new spending, adding $2.4 trillion to the deficit.

Senate Passage: Uncertain—possible via reconciliation with a 53-47 GOP majority, but fiscal hawks, Medicaid concerns, and Democratic opposition pose risks. A July 4, 2025, deadline adds pressure.

Revised Bill (20% Cut): Gross impact reduced to $720 billion (from $3.8 trillion), with tax cuts mostly removed (except a $500 billion placeholder), spending cuts at $1.2 trillion, and new spending at $220 billion, yielding a $480 billion deficit reduction.

introducing the Starter Guide to SF — a free wiki for any founder new to or considering moving to SF.

Charles McGonigal the corrupt FBI agent who was one of the major orchestrated of the Russian collusion hoax was convicted of BRIBERY and MONEY LAUNDERING When he should have been convicted of ESPIONAGE

If open ai never released 4o and waited to release 4.5 after 4 and released it with o3 instead of o1. Nobody would be saying we hit a wall. Literally no one.

The only reason people assume is because open ai ships so frequently that even when the updates are 30%-300% better on…

Starting today, all Perplexity users have access to SEC data across Search, Research, and Labs.

Our new SEC/EDGAR integration provides direct access to comprehensive financial data for all investors, making technical documents instantly understandable. pic.twitter.com/J9gc8A04h0

Important: Irony just died: Pakistan is appointed vice chair of United Nations Security Council Counter Terrorism Committee.. and chair of Taliban Sanctions Committee. What does this say about UN commitment to root out terror or frankly about our foreign policy clout in global…

— Rajdeep Sardesai (@sardesairajdeep) June 5, 2025

talking to a founder today who spent 3 years building community before launching product. smart. your tribe becomes your moat.

— Martin Tobias (Pre-Seed VC) (@MartinGTobias) June 5, 2025

"Budget Deficits Are Beautiful!" — A Trumpian Parody

From the desk of Donald J. Trump, 47th (and greatest) President, King of Golf, Builder of Walls, and now Self-Proclaimed Budget Deficit Whisperer.

My fellow Americans — and especially my fellow billionaires —

People always ask me, "Sir, how do you feel about trade deficits?" And I tell them, "TERRIBLE. Disgusting. Just the worst. They're like losing at golf to Rosie O’Donnell." We are LOSING to China. We send them money. They send us wind-up toys and TikToks. SAD!

But budget deficits? Let me tell you — budget deficits are a whole different story. Budget deficits are patriotic. They are strong, masculine, and they love America. I call them Freedom Holes — the deeper we dig, the freer we are. You heard it here first.

Look, people say, “But Mr. President, aren’t budget deficits connected to trade deficits?” WRONG. Fake news. Totally different. Completely unrelated. Just because the government borrows trillions and that increases imports doesn’t mean it’s my fault. That’s Econ 101 from the Deep State. I got a degree in Real Estate, which is basically economics plus golden toilets.

When I was president, I CUT taxes for rich people — HUGE success — and spent like a contestant on The Apprentice with a black Amex card. It was perfect. We made America great again on credit! You know who else loved deficits? Reagan. And he had the BEST hair before me.

They said, “Sir, the budget deficit is skyrocketing!” I said, “Skyrocketing? That’s what rockets do! Elon loves rockets. I love Elon. Therefore, I love budget deficits. SIMPLE.”

If you want to reduce trade deficits, they say, you should reduce budget deficits. But why would I reduce budget deficits when I can just blame China? It’s all China’s fault. Or windmills. Or Sleepy Joe. Anyone but me.

In conclusion, TRADE deficits are BAD, because they make us look weak. BUDGET deficits are GOOD, because they make me look generous. And looking generous gets me votes. And votes are like dollars, but better — you can’t file for bankruptcy on them. (I checked.)

Thank you. God bless America. And God bless the sacred art of debt.

– DJT "The only man who ever made default sound like a business plan."

“Donald Trump vs. The Smug Economist” — A Parody Dialogue

Scene: Mar-a-Lago. Gold walls. Gold chairs. Gold Diet Coke button. Trump sits behind a comically large desk. Enter: Dr. Deborah Knowitall, an Ivy League economist with three PhDs and zero tolerance for nonsense.

Dr. Knowitall:

Mr. Trump, with all due respect, your obsession with trade deficits while ballooning the budget deficit makes no economic sense.

Trump:

Wrong! Totally wrong. I’m like a genius. Stable. Very stable. Trade deficits are when we’re LOSING. Budget deficits? That’s called winning with style.

Dr. Knowitall:

Sir, they are connected. A government that spends more than it collects increases national savings shortfalls, which are offset by capital inflows. That drives up the dollar and worsens the trade deficit. Basic macroeconomics.

Trump:

Listen, Debra—

Dr. Knowitall:

Deborah.

Trump:

Debbie, here's the thing. When I was in office, we had the best deficits. Incredible deficits. Tremendous. I added trillions and the stock market loved it! You ever see the Dow with Obama? Sad. With me? BOOM.

Dr. Knowitall:

You added $7.8 trillion to the debt in one term. That’s more than any president in history. And you claim to hate debt!

Trump:

Only when other people do it. When I do it, it’s leverage. I wrote The Art of the Deficit. Beautiful book. Didn’t read it, but still.

Dr. Knowitall:

So to reduce trade deficits, you could have just... reduced government spending?

Trump:

Or — OR — I could slap tariffs on everyone, insult Canada, call China names, and sign my name really big on documents that do nothing. Which I did. You’re welcome.

Dr. Knowitall:

So you’re saying trade deficits are bad optics, but budget deficits are... campaign strategy?

Trump:

Exactly! Finally, she gets it! Trade deficits make us look weak. Budget deficits? No one understands them. They're invisible! Like calories in Diet Coke.

Dr. Knowitall:

This is why economists cry in the shower.

Trump:

Cry all you want, Debbie. The base loves a big, beautiful deficit — as long as I’m the one spending it. It’s not economics. It’s theater. And I always play the hero.

[Cue “Hail to the Chief,” played by Kid Rock on electric guitar.]

Dr. Knowitall:

We’re doomed.

Trump:

We’re winning. TREMENDOUSLY.

“Donald Trump Explains Inflation… With a Big Mac” — A Parody Sequel

Scene: Fox News Town Hall. A patriotic backdrop of eagles, flags, and golden arches. Trump takes the stage to a standing ovation. Sean Hannity moderates. An audience member, Tim from Ohio, nervously raises his hand.

Tim (audience member):

Mr. President, I love you, sir. But everything is more expensive now. Groceries. Gas. Even Big Macs! Is that inflation? And… didn’t deficits make it worse?

Trump:

Great question, Timmy. Beautiful question. Probably the best question anyone’s ever asked in the history of questions. And yes — Big Macs. Let’s talk about it.

[Trump adjusts his tie, leans forward like he’s about to drop wisdom on the world.]

Trump:

When I was president, a Big Mac cost $3.99. Now? It's, what, $6.99? That’s not inflation. That’s Bidenflation. Okay? That’s Sleepy Joe putting ketchup on the economy and calling it a sauce.

Hannity:

So you're saying... prices are up because of Biden?

Trump:

Of course! Look, under me, we printed a lot of money. Like, a LOT. But it was the right kind of printing. Smart printing. Gold-standard-level printing. Okay?

Tim:

But sir… isn’t that what causes inflation?

Trump:

No, no. See, when I print money, it’s Trump Money. It’s strong. Masculine. Like a Big Mac with three patties. Biden prints money, and it’s soy money. Very weak. Like a sad little McChicken.

Hannity (nodding, confused):

Interesting.

Trump:

It’s all about confidence, Sean. I walk into a McDonald's and inflation goes down out of respect. When Joe walks in, the Filet-O-Fish hides in shame. Even the fries go limp.

Tim:

But... deficits?

Trump:

Let me tell you about deficits, Tim. Deficits are like extra cheese. You don’t need it. But it makes the burger better. Unless you’re lactose intolerant. Which is what Democrats are — lactose intolerant socialists. They hate flavor, they hate America, and they hate cheese.

Hannity:

And what about the national debt?

Trump:

It’s like the calories on the Big Mac box. Nobody reads them. Just vibes.

[Crowd erupts. Trump throws MAGA hats. A bald eagle cries in the distance.]

Tim:

So… inflation is fake?

Trump:

No. Inflation is real. But it’s Biden’s fault. And possibly China’s. Or windmills. We’re looking into it. But don’t worry — when I’m back, I’ll fix inflation with volume. I’ll negotiate with McDonald’s directly. We’ll get Big Macs for $1 again. Two for $2. Maybe three for $3 if I feel generous.

Hannity:

You heard it here, folks. Big Macs, back on budget — Trump style.

Trump: Make America Eat Again.

“Donald Trump Explains the Federal Reserve… Using a Golf Course” — A Parody

Scene: Trump National Golf Club, Bedminster. Sun is shining. Birds are chirping. A caddy stands by nervously holding a gold-plated 9-iron. Trump is in a red “Make Rates Low Again” hat, giving an impromptu “economic seminar” to a group of very confused donors.

Trump (squinting over the fairway):

Okay, folks. Today I’m going to explain something very important. Very mysterious. The Federal Reserve. Some say it controls interest rates. Others say it's just a bunch of bankers with boring voices. But really, it’s just like a golf course. My golf course.

Donor 1:

Sir… the Fed is supposed to be independent.

Trump:

Wrong! FAKE NEWS! The Fed is supposed to do what I tell them. They’re like my caddy. I say “9-iron,” they don’t hand me a putter. Jerome Powell didn’t get that memo. Sad!

[He swings. Slices the ball into a water hazard.]

Trump:

Okay, maybe that was a bad lie. But here’s the deal. Interest rates are like greens fees. You keep them low, more people show up to play. The economy thrives. Everyone’s buying golf carts. Big success!

Donor 2 (cautiously):

And if rates go up?

Trump:

Then it’s Biden’s course. And he raised the fees so high, no one wants to play. Except maybe China. And they're cheating. Believe me.

Donor 3 (trying to follow):

So… the Fed adjusts rates to slow inflation?

Trump:

That’s what they say. But what they really do is panic. Like a golfer with the yips. Powell kept raising rates like he was trying to hit the moon. TERRIBLE. Made housing unaffordable. Destroyed the vibes. Nobody wants to build condos next to a course where the Fed’s hiking.

Donor 1:

But didn’t inflation spike after you did all that pandemic stimulus?

Trump (waving it off):

Stimulus is like a free cart ride. Everyone loves it. You want to slow down the economy? Just put a windmill on hole 7. Works every time.

Donor 2:

But shouldn’t the Fed be neutral?

Trump:

Neutral? No. I want a Fed that’s aggressive. Like a great caddy with killer instincts. One that whispers, “Mr. President, sir, the green is yours. We’ll keep rates LOW so you can swing freely and take ALL the credit.”

[He dramatically points to the horizon.]

Trump:

In my second term, I’ll redo the whole system. No more boring bankers. I’ll replace Powell with someone who understands golf and growth. Maybe Phil Mickelson. Or Kid Rock. We’re exploring options.

Donor 3:

So how would you describe the Fed, in one sentence?

Trump (smirking):

The Fed is like the clubhouse bartender — nice to have around, but don’t let him touch the cart keys.

[Cue dramatic music. A bald eagle circles overhead. Somewhere, an economist collapses in a heap of tears and spreadsheets.]

“Donald Trump Explains Cryptocurrency… Using Monopoly Money” — A Parody

Scene: A gold-plated conference room at Trump Tower. Red velvet curtains. A giant portrait of Trump hugging a Bitcoin. The audience includes tech bros, confused seniors, and one guy in a Doge costume. Trump struts in holding a stack of Monopoly bills and a physical Bitcoin he bought on eBay.

Trump:

Alright, folks. Let’s talk crypto. Everybody’s asking me, “Sir, what is cryptocurrency?” And I tell them, very simply — it’s Monopoly money for people who think they’re smarter than the Federal Reserve.

[Holds up pink Monopoly $500 bill.]

This right here? This is basically Dogecoin. It's fake, but fun. You buy it, you lose it, maybe you buy a hotel on Baltic Avenue, and then your cousin Gary starts calling himself a 'blockchain strategist' on LinkedIn. It’s a whole thing.

[Audience laughs nervously.]

But listen, when I was president, Bitcoin was low. Why? Because the world was STABLE. When the world is confused, when it’s scared, when it smells like Joe Biden’s economy, crypto goes UP. People run to digital fake money because they’re tired of real fake money.

Tech Bro (from the crowd):

But sir, crypto is decentralized.

Trump:

Decentralized? That means no one’s in charge. That’s terrible. You know what else was decentralized? Occupy Wall Street. And they all smelled like armpits and bad ideas.

Senior in the back:

Can I use Bitcoin to buy soup?

Trump: Great question. No. You can’t. You buy Bitcoin to feel smart and poor at the same time. It’s like art, but without the canvas. Or the talent. Or the actual object.

Dogecoin Guy:

What about Doge?

Trump:

Doge? Doge is a MEME. It’s like if Garfield and Chuck E. Cheese had a digital baby and Elon Musk baptized it on Twitter. And I respect that! I do. Tremendous branding. Terrible currency.

[He holds up a shiny TrumpCoin prototype.]

Now THIS… this is what crypto should look like. It’s called TrumpCoin™. Backed by pure American confidence. No blockchain. Just my face on the front, and your dreams on the back.

Audience gasps.

Trump:

You can use TrumpCoin to buy steaks, enroll at Trump University 2.0, or reserve a seat on the Trump Moon Resort coming in 2028. Maybe.

Tech Bro:

But what’s the tech behind it?

Trump:

Tech? No need. Just vibes. And a gold sticker.

[He slaps the gold “T” on the Monopoly box.]

Trump:

Crypto, folks, is like Monopoly. Most people play, few people win, and the banker always cheats. That’s why I love it. That’s why I fear it. That’s why I tried to ban it but also secretly bought some. Smart move. Great hedge.

[Music swells. He tosses Monopoly bills into the crowd like it’s a strip club of economic confusion.]

Trump:

Thank you. Buy TrumpCoin. Dump Doge. And remember: if money’s fake, at least let it have a good haircut.

“Donald Trump Explains Climate Change… Using Air Conditioning” — A Parody

Scene: Trump rally in Arizona. It’s 114°F. Trump is under a giant fan wearing a suit too heavy for the desert and sipping Diet Coke. There’s a sweating crowd, a podium, and a very confused climate scientist in the front row holding a “PLEASE” sign.

Trump (wiping his brow dramatically):

Okay, folks — it’s HOT. You feel it. I feel it. But that doesn’t mean it’s climate change. That means we need better air conditioning. Big AC. The best AC.

[Crowd cheers “A-C! A-C! A-C!”]

They say the planet is warming. I say — turn the thermostat down! It’s not complicated! You don’t ban cows. You don’t drive tiny electric cars that look like golf carts made by communists. You call Carrier, you crank it to 62, and BOOM, problem solved.

Climate Scientist (yelling):

That’s not how any of this works!

Trump (ignoring):

Look, I know weather. I’ve played golf in all kinds. Rain. Wind. Hurricane-level conditions. One time, I played through a tornado in Nebraska — got a birdie. True story. And let me tell you: weather is different than climate. Weather is what you wear. Climate is what liberals whine about on TikTok.

[Crowd: “LOCK UP THE WEATHER!”]

Trump:

They want to ban gas stoves, folks. Gas stoves! I love gas stoves. You can’t make a proper Trump Steak on an electric grill. That’s like trying to win a trade war with feelings. It doesn’t work.

Climate Scientist (meekly):

But sir… the oceans are rising.

Trump:

So we build taller sea walls! It’s called innovation! Florida’s going underwater? Fine. We just make New Florida™ on top of the old Florida. Stack it like Trump Tower.

[Crowd begins chanting “STACK! STACK! STACK!”]

Trump:

They say fossil fuels are bad. But when I take Air Force One over a coal plant — beautiful smoke. Gorgeous clouds. That’s American industry. That’s not pollution — that’s freedom steam.

Climate Scientist (head in hands):

Oh God.

Trump:

And windmills? Windmills kill birds. I love birds. I just don’t want them chopped up by Biden’s death fans. Also, they give you cancer. Probably. We’re looking into it.

[He points at the sun.]

Trump:

THAT is the problem. Too bright. Too aggressive. When I’m back in office, we’re gonna talk to the Sun. We’re gonna renegotiate. Maybe a few days off a week. Maybe part-time sun.

[Crowd roars. An American flag unfurls in the shape of a snowflake.]

Trump:

So don’t let the climate hoaxers fool you. The real solution is simple: More air conditioning. More Trump. Less Greta.

Crowd: “COOL IT DOWN! BUILD THE DOME!”

Whatever.

Keep the EV/solar incentive cuts in the bill, even though no oil & gas subsidies are touched (very unfair!!), but ditch the MOUNTAIN of DISGUSTING PORK in the bill.

In the entire history of civilization, there has never been legislation that both big and beautiful.…

:max_bytes(150000):strip_icc()/GettyImages-848755326-48dd2711646247648c4faebc98715119.jpg)